January 4, 2023

Apple Stock: You’ve Been Warned Again

Since mid-December 2021, I have followed Apple Inc. (NASDAQ AAPL). Since then, I have maintained neutrality, saying that the stock was too expensive despite its historical multiples and the fact that it generates free cash flow (“FCF”), which has allowed the company to continue to please shareholders in difficult times.

My last article, ” How Apple’s Moonshot is Not Likely in 2023“, discussed the danger of disruption to demand that could threaten the company.

The price elasticity of Apple’s products is under serious threat, despite the brand power. As 24.1% of Apple’s total revenue is dependent on Europe [as of FY2022], gas prices and electricity bills have risen twice. So, amid China (18% AAPL’s revenues), where the situation is not improving in its own right, I expect a demand disruption. It’s difficult to track with just lead times.

This risk has been increasing over time. I’ll discuss the latest news and how it might impact you in today’s article.

WCCFTech published a December 30 article stating Apple’s intention to reduce the price of the iPhone 15 and the larger iPhone 15 Plus next year due to lower demand.

According to the company’s 10-K, Apple generated 52% of its total revenue in FY2022, which was around 52% in the most recent quarter. It’s unclear how much of that revenue came primarily from iPhone 14 and iPhone 14 Plus models. Therefore, it’s difficult to draw any conclusions about the effect of price cuts in just 2 categories. As of FY2022, two categories account for 50% of this segment’s total assortment. Therefore, I believe the price reduction – if it occurs – will have a significant impact on the first half of the sales equation (price multiplied by total volume = Total Sales).

For a while, the fact that Apple has some problems with its “Plus” models was discussed. Few believe that Apple will have to lower the price of the “Plus” model, but it may also be necessary to lower the price for the flagship model. If Apple reduces the price for the iPhone 15 Plus from $800 to $800, then the standard iPhone 15 will likely cost $800. This means that the iPhone 15’s price would need to drop to $700 in order to maintain a price differential between the two models.

This example shows how disinflationary events, about which the market was so happy not long ago can prove disastrous for large companies that have maintained a “high base” but that experience not only a slowdown of sales growth but also a lack thereof in times when there is declining demand.

Even though Apple doesn’t have to lower its prices it will lead to a decrease in revenue and EPS.

As I mentioned earlier, Apple’s products are very price-elastic – so it is possible that Apple will need to decrease production volumes in order to offset lower selling prices. The stock will likely continue to fall if this happens.

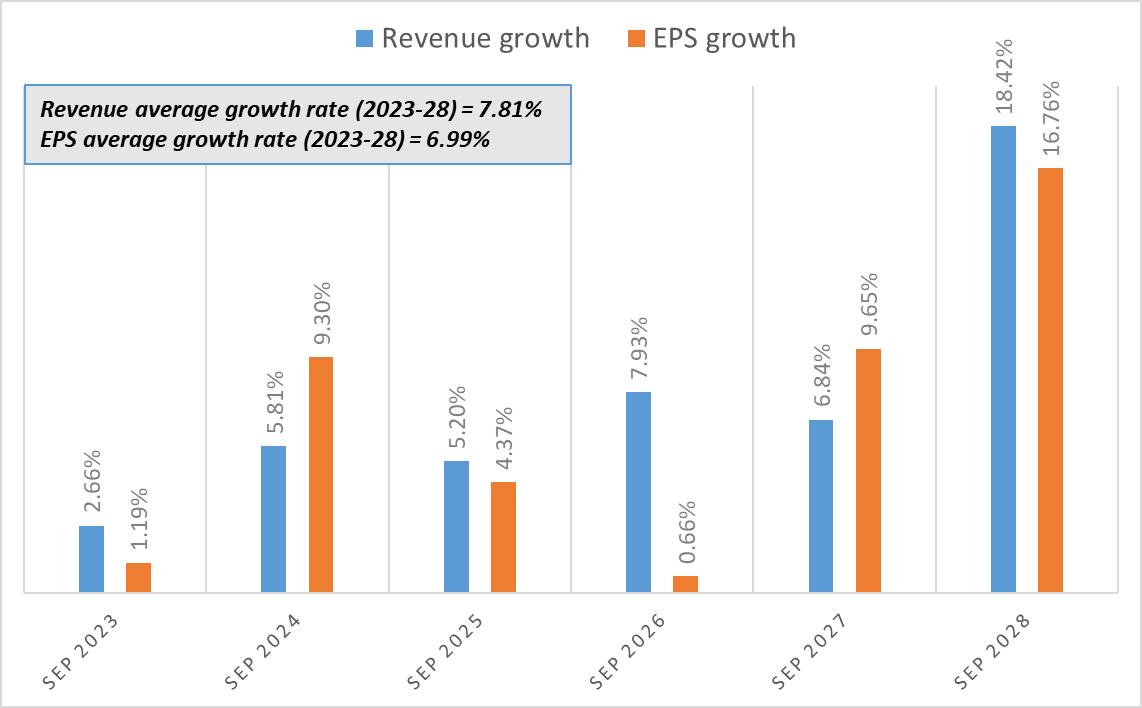

Analysts believe that the company will not see a decrease in earnings per share and revenue in FY2023. According to 38 Wall Street professionals Apple and ESP revenues will rise by 2.66% (year-over-year) respectively. Additionally, FY2024 will mark a significant recovery period. In 2028, we will experience growth rates more than 2x longer-term averages, according to one analyst.

Author’s Excel calculations, Seeking Alpha data

It is unclear how the company will achieve these goals considering the demand dynamics. The Street remains too optimistic about the company’s long-term prospects, despite the 37 downward EPS revisions over the past three months.

It seems like everyone is not learning from the mistakes of the past. You might want to take a look at some.

Apple saw a drop in demand for its products in 2016. According to ROIC.ai, the revenue and EPS fell 7.7% and 9.9% respectively (YoY), and the EBIT margin dropped 27 basis points. The company traded at an average price/earnings ratio (of 12.4x), which was approximately 0.6 times that of the S&P 500 Index.

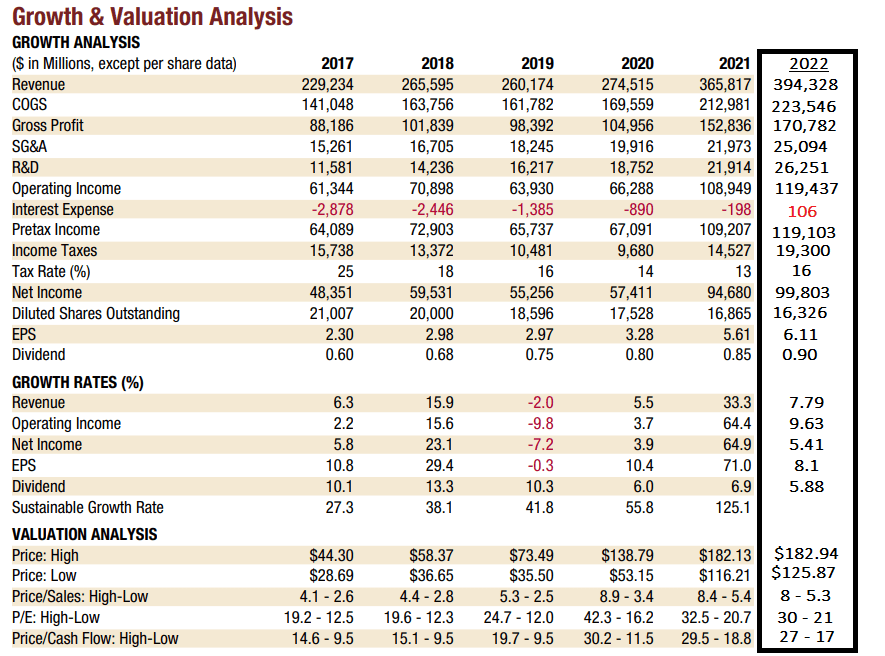

2019 is a fresher example. The company’s earnings per share and revenue declined by 2% and 9.8%, respectively (YoY), while the EBIT margin fell 21 basis points. This year, [FY2019] has been included in Argus‘s analytic table which includes all key multiples averaged for the period.

Author’s notes for Argus Equity Research, AAPL

AAPL’s 2019 average price-to-earnings ratio was 17.3x. This was approximately 0.7 times the S&P 500 Index.

What will we see in 2022?

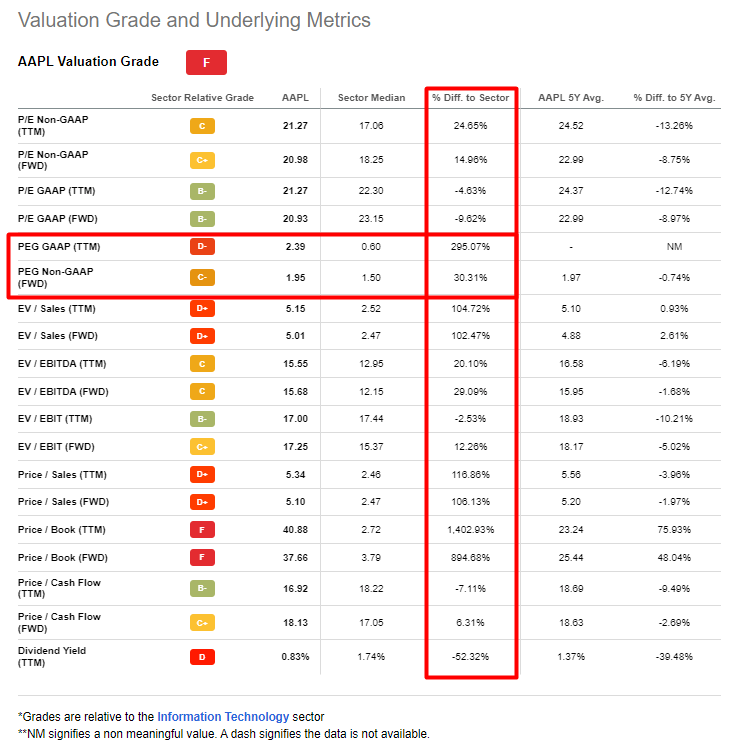

Apple stock trades at a substantial premium to its 2016 and 2019 multiples. This ranges from 15%-30% depending upon the multiple being compared.

AAPL’s corporate growth forecasts for next year are so low that it cannot justify such high multiples – regardless of how large its moat. The excess of PEG ratio demonstrates this.

Seeking Alpha, AAPL’s Valuation, author’s notes

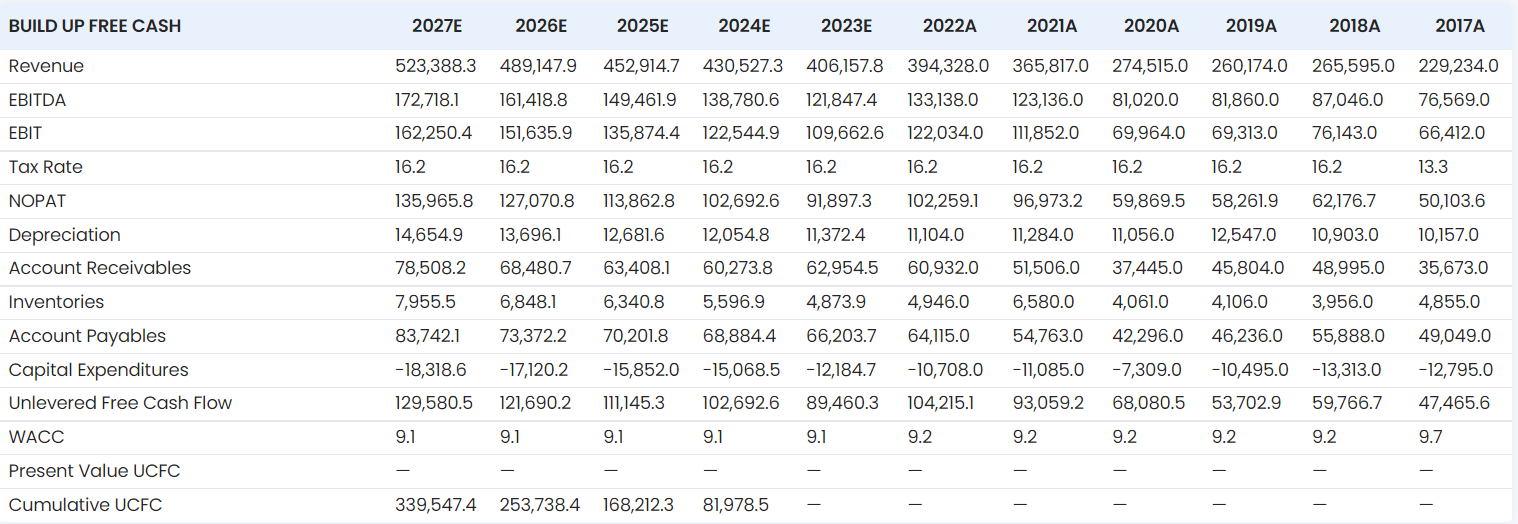

Let’s talk about business valuation while we’re on the topic. I simply take the consensus forecasts and input them into a DCF model. I expect that EBITDA and EBITDA margins would again decline in FY2023 (by 27% and 30% respectively), but will recover in 2024, and be close to the previous years’ records at the end of the forecast period (FY2027: 31% and 33%).

In FY2023, the ratio of CAPEX and sales will drop slightly to 3%. I expect capital allocation to be more conservative in the face of all these difficulties. The company will return to 3.5% as it was in 2024.

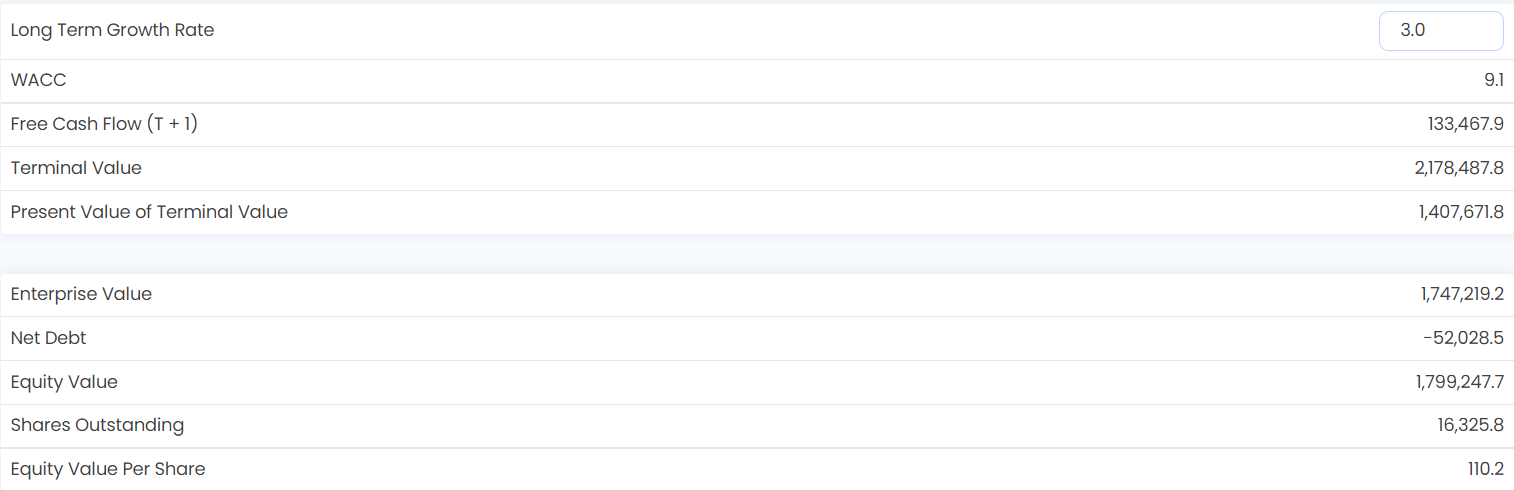

It is difficult to calculate the WACC because it is subjective and involves many unreliable assumptions. With a market premium of 4.7%, I take a 3.7% risk-free rate (10-year US bonds). We get a WACC of 9.1% with a beta of 1.

These are the main conclusions of the model.

Stratoshere.io author’s inputs

If we assume long-term corporate growth of 3% (Gordon’s g model), then equity value net of net debt is $ 1,799 billion – or about $110.2 per share. Even with optimistic forecasts, we see an overvaluation at about 12% relative to yesterday’s closing prices.

Stratoshere.io author’s inputs

This downside potential is even greater if actual sales and earnings figures are not consistent with the current pricing.

AAPL outperformed its peers in the tech sector selloff of 2022, though the stock remains in the red. AAPL’s sector-leading performance in 2021 was rare. The company has been a “last resort” for investors who don’t want to take on too many risks. This has led to a premium that could stay with AAPL longer than logic would have me believe. This is a significant risk given my findings about Apple’s overvaluation.

The stock is also >31% below its multi-month local high. This could indicate that AAPL has priced into all of the negative aspects discussed above.

The reliability of the information that the company may be considering lowering its flagship 15-series products is another risk. Yyeux1122 did not share this information via Naver. This user previously leaked information that accurately predicted the price, color, and chip of the iPhone 14 Pro. It also revealed the design changes and release date for the tenth-generation iPad. There is now a chance that the leak may not be accurate.

The above information leads me to conclude that both the possible price drop for iPhone 15 and the fall in sales volumes should eventually result in the multiple contractions I often refer to in my articles on Apple. DCF simulations support this conclusion. They show that AAPL is still too expensive [despite its moat] even though it has very optimistic consensus forecasts. The company’s unique advantage, which Jim Kelleher, CFA at Argus Research described as a constantly updated roster of highly sought-after products, will allow it to overcome major problems. This does not necessarily mean that you should buy AAPL now. We may find more attractive entry points for the future. Therefore, I am neutral and have set a target price of $110 per share for 2023. My thesis is confirmed by the ugly-looking stock chart of AAPL.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}